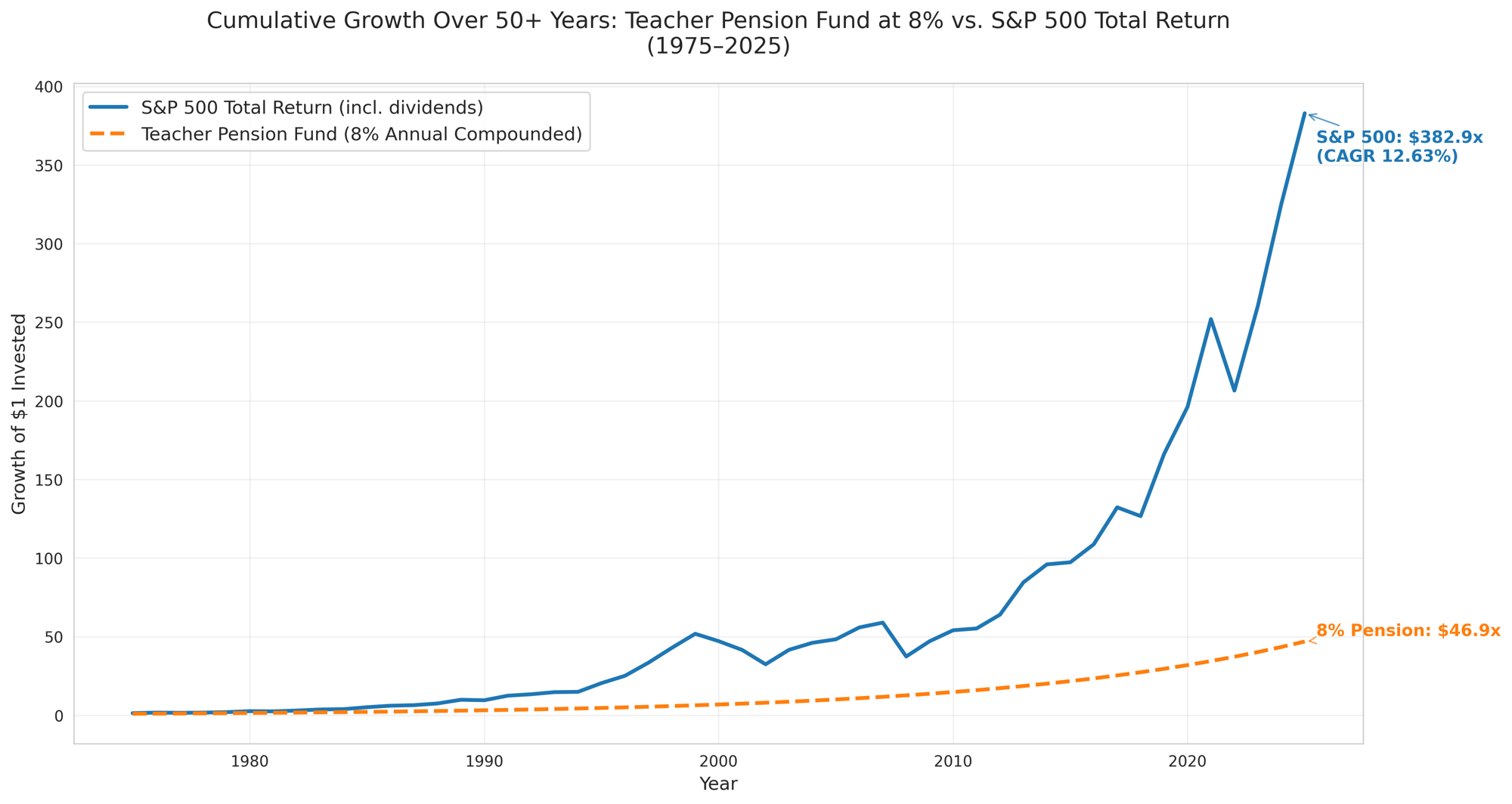

Teacher pension funds, typically defined-benefit plans, were designed decades ago for stable, lifelong careers in one state or district. They fail to prepare for modern 50+ year careers (spanning multiple jobs, states, or even professions) due to structural flaws. They also buy the bonds that finance the construction of buildings where the teachers work.

Benefits are heavily backloaded: little value accrues early in a career, with most wealth spiking only after 20–30 years tied to final average salary and service years. Teachers leaving before vesting (often 5–10 years) get back only their contributions, sometimes with minimal interest — no employer match.

Portability is poor; pensions rarely transfer across state lines, penalizing mobility. Many teachers never reach full benefits, as turnover is high — over half leave before qualifying for meaningful payouts, while plans assume only a minority stay long-term.

Early retirement incentives (often after 25–30 years) encourage exiting in one’s 50s, not sustaining decades-long work. Unfunded liabilities divert contributions to debt rather than future benefits. Overall, these systems reward narrow, traditional paths but leave flexible, long careers underprepared, forcing reliance on personal savings or Social Security where available.

Stay informed! NCTR members, register today at https://t.co/dVuYd5tSn2 pic.twitter.com/Cn9CTGXoKn

— National Council on Teacher Retirement (@NCTRtalk) February 12, 2026

The Teachers Insurance and Annuity Association (TIAA) was founded in 1918 by philanthropist Andrew Carnegie through the Carnegie Foundation for the Advancement of Teaching. In 1905, Carnegie had established a free pension system for college professors, but it proved unsustainable as higher education expanded rapidly. To create a permanent, portable solution, the Foundation launched TIAA as a nonprofit life insurance company, with Carnegie Corporation providing a $1 million endowment.

TIAA offered contributory, fully funded annuities where both employers and employees shared costs, ensuring secure retirement income for educators—predating Social Security. In 1952, it added CREF (College Retirement Equities Fund), the first variable annuity, to combat inflation. This innovative model focused on lifetime income for those serving academia.

$

Fidelity does not offer a traditional “teacher pension plan.” Instead, it provides 403(b) retirement savings plans, which are the most common supplemental retirement option for K-12 teachers and higher-education employees across the USA.A 403(b) plan allows educators to contribute a portion of their salary on a pre-tax basis (or Roth after-tax), reducing current taxable income while building retirement savings. Contributions grow tax-deferred, and investments can include mutual funds, target-date funds, and other options managed through Fidelity.

Unlike state teacher pensions (defined benefit), Fidelity’s 403(b) is a defined contribution plan — the final amount depends on contributions and investment performance. It supplements a teacher’s primary state pension and Social Security.

Fidelity is one of the largest and most respected 403(b) providers, known for low-cost investment options and strong online tools. Availability depends on whether your school district has selected Fidelity as an approved vendor.